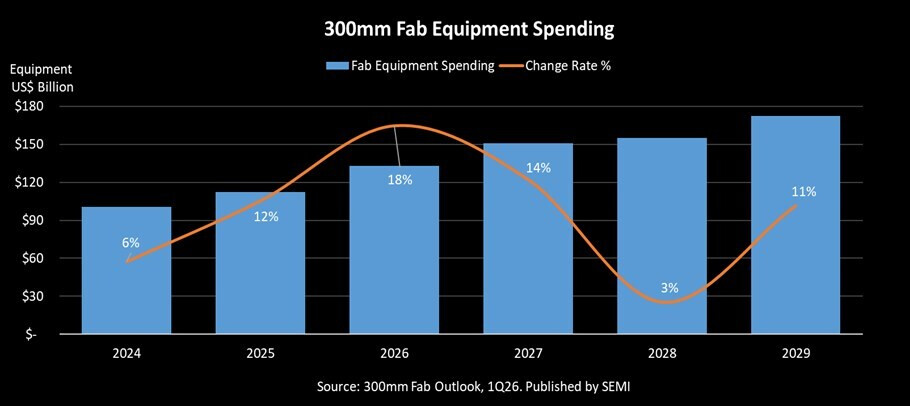

The semiconductor industry is entering a period of sustained investment growth, with global 300mm fab equipment spending expected to climb 18% in 2026 before reaching $151 billion by 2027. This surge reflects the industry's response to AI-driven demand and the push toward localized manufacturing ecosystems.

Looking ahead, the Logic & Micro segment will lead with cumulative investments of $228 billion from 2027 to 2029, primarily driven by foundry sector expansion and sub-2nm capacity additions. Advanced node technologies are critical for AI performance improvements and power efficiency, setting the stage for a new wave of high-performance chips.

Memory equipment spending is also projected to rise, with DRAM and 3D NAND investments totaling $173 billion over the same period. High Bandwidth Memory (HBM) demand from AI training and storage capacity needs for model inference will sustain this growth cycle.

Regionally, China, Taiwan, Korea, and the Americas will see substantial spending, supported by government incentives and supply chain localization efforts. Japan, Europe & Middle East, and Southeast Asia are also expanding investment, though from smaller bases.

The report highlights 404 global facilities and lines, with 198 updates and 9 new projects since its last publication. This reflects the industry's commitment to advanced capacity and resilient supply chains as it transitions into the AI era.