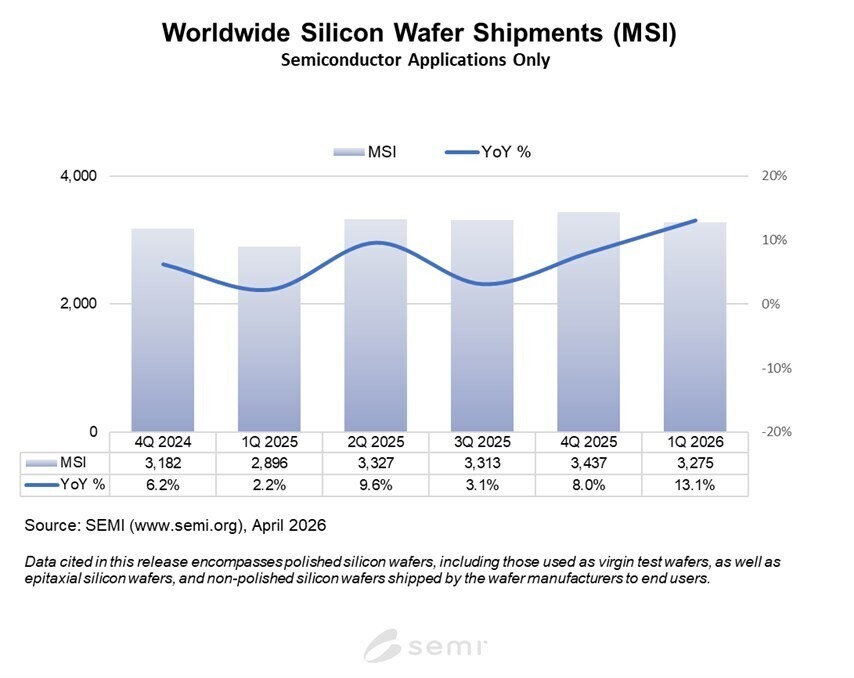

Silicon wafers are seeing a sharp rebound in production, but the recovery is not uniform across industries. The latest data shows worldwide wafer shipments climbed 13.1% year-over-year in Q1 2026, totaling 3,275 million square inches—a figure that reflects surging demand from AI data centers for advanced logic and memory chips. However, this growth comes with a catch: while AI infrastructure is benefiting from expanded silicon capacity, consumer electronics—particularly smartphones and PCs—are feeling the strain of constrained high-bandwidth memory (HBM) supply.

This imbalance is reshaping the semiconductor landscape. Industrial segments are seeing stronger performance, helping clear excess inventory, but consumer markets are lagging due to HBM being prioritized for AI workloads. The result is a market where silicon production is rising, yet memory bottlenecks persist, potentially slowing advancements in consumer hardware.

- Wafer Shipments: 3,275 million square inches (Q1 2026), up 13.1% year-over-year

- Quarterly Decline: 4.7% drop from Q4 2025, following seasonal trends

- Key Drivers: AI data centers (logic/memory), power management devices

The shift toward AI-driven silicon is evident in the allocation of HBM modules, which are critical for high-performance computing but increasingly scarce for consumer devices. This dynamic suggests that while new GPUs and CPUs may be ramping up in production, the availability of high-capacity RAM—especially HBM—could continue to limit performance gains for gamers and PC enthusiasts.

Silicon wafers serve as the foundation for most semiconductors, ranging from 200 mm to 300 mm in diameter. The recent uptick in production indicates that foundries are scaling up capacity to meet demand, particularly for AI-related applications. However, the uneven recovery highlights that while silicon supply is improving, memory bottlenecks remain a critical hurdle for consumer electronics.

The broader trend points to a market where AI infrastructure is taking precedence over consumer hardware improvements. This could delay advancements in PC and smartphone performance until HBM capacity can be expanded further. For now, the industry faces a dual challenge: balancing the surge in silicon production with the persistent memory constraints that are holding back non-AI segments.

The question remains: how long will these bottlenecks persist? If new HBM capacity cannot be brought online quickly enough, the gap between AI-driven silicon advancements and consumer hardware improvements may widen further.